Hedley Widdup

Fund Manager – Lion Group

On average, the market is always right. BUT, for miners, the height of booms and nadir of the bust is where the market overshoots driven by extremes of sentiment, and at these times the market for miners is neither rational nor efficient. IE – it is Wrong. The loftier the boom and the deeper the bust, the more extreme the market overshoots. The “stronger for longer” mining boom from 1998-2008 was exacerbated by economic stimulus between 2009-2011, which along with weakening commodities led to a severe extended mining bust from 2011-2015. Previous busts have seen major miners, with best in class costs and cash flows, able to take advantage of discounted opportunities – providing liquidity into weakness and arresting the fall. However, this bust caught the major miners (as a group) with extreme debt levels and digesting peak priced acquisitions, so they not only fed the bust with discounted project sales, they were the feature of capitulation selling in 2015. As a result, this bust in particular saw miners severely oversold to a weighting in the market well below previous busts.

2016 saw a strong swing back to miners, as investors bought up major miners and gold producers. Indices bounced strongly, which is historically unusual for early in a boom. Despite this, market weightings have only just returned to levels that are consistent with start of other booms.

Bust periods create opportunity in two ways:

- Falling equity prices – everything becomes cheaper, and eventually discounts emerge. Long falls create deep discounts. The 2011-2015 bust was so long and deep, and despite a recent flurry in the indices, many micro-cap and junior miners and aspirants still trade on depressed valuations.

- Project development pipeline neglected as miners go on a capital expenditure strike. Short busts create a short pause in project development, but big busts create a long gap – and development assets therefore become much more attractive later in the cycle.

Gold equities benefited from industry best costs and a robust metal price in 2016. During 2017, the creeping realisation that Donald Trump would not provide the bureaucratic panacea for the US economy that the market expected has shifted expectations of interest rates and gold has gained robustness as a result. Gold equities should reflect this, but fund rebalancing by a major US gold producer ETF (the GDXJ) has resulted in gold equities temporarily underperforming the metal. This presents an opportunity in itself.

Status of the BOOM:

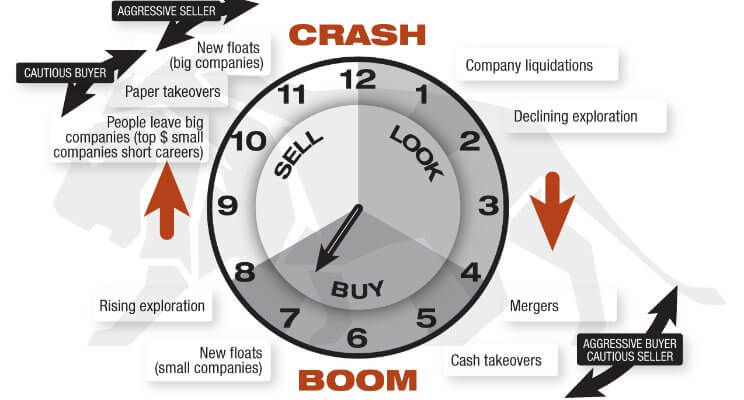

- The Lion Clock remains at 7 o’clock. The IPO market has re-opened but we are still waiting for exploration to turn from a negative to positive trend.

- Miners are in early boom phase. Index recovery so far is historically unusual, and reflects partial unwinding of extreme discounting of the bust

- The industry is buying again. After a long period of cutting expenditure, Reserves have shrunk and development pipelines dried up. Now that balance sheets are back under control and healthy net cash has built up (particularly in gold producers) we are seeing major miners invest in, or bid to take over their smaller peers to re-stock their future production inventories. Gold equities depressed by the GDXJ effect present many lucrative potential targets, so there is a sense of looming M&A interest in gold, but the same dynamic is likely to play out across the broader industry.

- Likelihood of a robust boom. There has been a long capital strike, which will result in supply demand imbalances and project development pipeline will be slow to restart.

- Exploration is now restarting. Not yet enough activity to push costs up, but given time, will result in discoveries – which will have a stimulatory effect.

- Risk is mainly macro and not mining specific. The issues shaping investor concern are centred on monetary policy – interest rates have to increase, the big question is when. This will affect all equities, miners included, and miners comparative robustness will depend on commodity prices and industry cost structures when the adjustment takes place.